James S. Henry, the-american-interest.com [original article contains more charts/diagrams and illustrations]; via LJB; see final paragraphs for highlighted summary.

Re "shock therapy," mentioned by the author of this article, I'll never forget what I heard in Ukraine (93-95; was there as a U.S. dip) from friends/contacts there re Western "help": "In Ukraine, we got shock, but not therapy" (same could be said about Russia/the Russians in the 1990s/early 2010s); re Russian "hacking," see (for your amusement).

image (not from article) from [JB -- of the two couples, choose your favorite :)]

{kind=link}

Did the American people really know they were putting such a “well-connected” guy in the White House?

Throughout Donald Trump’s presidential campaign he expressed glowing admiration for Russian leader Vladimir Putin. Many of Trump’s adoring comments were utterly gratuitous. After his Electoral College victory, Trump continued praising the former head of the KGB while dismissing the findings of all 17 American national security agencies that Putin directed Russian government interference to help Trump in the 2016 American presidential election.

As veteran investigative economist and journalist Jim Henry shows below, a robust public record helps explain the fealty of Trump and his family to this murderous autocrat and the network of Russian oligarchs. Putin and his billionaire friends have plundered the wealth of their own people. They have also run numerous schemes to defraud governments and investors in the United States and Europe. From public records, using his renowned analytical skills, Henry shows what the mainstream news media in the United States have failed to report in any meaningful way: For three decades Donald Trump has profited from his connections to the Russian oligarchs, whose own fortunes depend on their continued fealty to Putin.

We don’t know the full relationship between Donald Trump, the Trump family and their enterprises with the network of world-class criminals known as the Russian oligarchs. Henry acknowledges that his article poses more questions than answers, establishes more connections than full explanations. But what Henry does show should prompt every American to rise up in defense of their country to demand a thorough, out-in-the-open congressional investigation with no holds barred. The national security of the United States of America and of peace around the world, especially in Europe, may well depend on how thoroughly we understand the rich network of relationships between the 45th President and the Russian oligarchy. When Donald Trump chooses to exercise, or not exercise, his power to restrain Putin’s drive to invade independent countries and seize their wealth, as well as loot countries beyond his control, Americans need to know in whose interest the President is acting or looking the other way.

—David Cay Johnston,

Pulitzer Prize-winning author of The Making of Donald Trump

“Tell me who you walk with and I’ll tell you who you are.”

—Cervantes

“I’ve always been blessed with a kind of intuition about people that allows me to sense who the sleazy guys are, and I stay far away.”

—Donald Trump, Surviving at the Top

Even before the November 8 election, many leading Democrats were vociferously demanding that the FBI disclose the fruits of its investigations into Putin-backed Russian hackers. Instead FBI Director Comey decided to temporarily revive his zombie-like investigation of Hillary’s emails. That decision may well have had an important impact on the election, but it did nothing to resolve the allegations about Putin. Even now, after the CIA has disclosed an abstract of its own still-secret investigation, it is fair to say that we still lack the cyberspace equivalent of a smoking gun.

Fortunately, however, for those of us who are curious about Trump’s Russian connections, there is another readily accessible body of material that has so far received surprisingly little attention. This suggests that whatever the nature of President-elect Donald Trump’s relationship with President Putin, he has certainly managed to accumulate direct and indirect connections with a far-flung private Russian/FSU network of outright mobsters, oligarchs, fraudsters, and kleptocrats.

Any one of these connections might have occurred at random. But the overall pattern is a veritable Star Wars bar scene of unsavory characters, with Donald Trump seated right in the middle. The analytical challenge is to map this network—a task that most journalists and law enforcement agencies, focused on individual cases, have failed to do.

Of course, to label this network “private” may be a stretch, given that in Putin’s Russia, even the toughest mobsters learn the hard way to maintain a respectful relationship with the “New Tsar.” But here the central question pertains to our new Tsar. Did the American people really know they were putting such a “well-connected” guy in the White House?

The Big Picture: Kleptocracy and Capital Flight

Afew of Donald Trump’s connections to oligarchs and assorted thugs have already received sporadic press attention—for example, former Trump campaign manager Paul Manafort’s reported relationship with exiled Ukrainian oligarch Dmytro Firtash. But no one has pulled the connections together, used them to identify still more relationships, and developed an image of the overall patterns.

Nor has anyone related these cases to one of the most central facts about modern Russia: its emergence since the 1990s as a world-class kleptocracy, second only to China as a source of illicit capital and criminal loot, with more than $1.3 trillion of net offshore “flight wealth” as of 2016.1

This tidal wave of illicit capital is hardly just Putin’s doing. It is in fact a symptom of one of the most epic failures in modern political economy—one for which the West bears a great deal of responsibility. This is the failure, in the wake of the Soviet Union’s collapse in the late 1980s, to ensure that Russia acquires the kind of strong, middle-class-centric economic and political base that is required for democratic capitalism, the rule of law, and stable, peaceful relationships with its neighbors.

Instead, from 1992 to the Russian debt crisis of August 1998, the West in general—and the U.S. Treasury, USAID, the State Department, the IMF/World Bank, the EBRD, and many leading economists in particular—actively promoted and, indeed, helped to finance one of the most massive transfers of public wealth into private hands that the world has ever seen.

For example, Russia’s 1992 “voucher privatization” program permitted a tiny elite of former state-owned company managers and party apparatchiks to acquire control over a vast number of public enterprises, often with the help of outright mobsters. A majority of Gazprom, the state energy company that controlled a third of the world’s gas reserves, was sold for $230 million; Russia’s entire national electric grid was privatized for $630 million; ZIL, Russia’s largest auto company, went for about $4 million; ports, ships, oil, iron and steel, aluminum, much of the high-tech arms and airlines industries, the world’s largest diamond mines, and most of Russia’s banking system also went for a song.

In 1994–96, under the infamous “loans-for-shares” program, Russia privatized 150 state-owned companies for just $12 billion, most of which was loaned to a handful of well-connected buyers by the state—and indirectly by the World Bank and the IMF. The principal beneficiaries of this “privatization”—actually, cartelization—were initially just 25 or so budding oligarchs with the insider connections to buy these properties and the muscle to hold them.2 The happy few who made personal fortunes from this feeding frenzy—in a sense, the very first of the new kleptocrats—not only included numerous Russian officials, but also leading gringo investors/advisers, Harvard professors, USAID advisers, and bankers at Credit Suisse First Boston and other Wall Street investment banks. As the renowned development economist Alex Gerschenkron, an authority on Russian development, once said, “If we were in Vienna, we would have said, ‘We wish we could play it on the piano!'”

For the vast majority of ordinary Russian citizens, this extreme re-concentration of wealth coincided with nothing less than a full-scale 1930s-type depression, a “shock therapy”-induced rise in domestic price levels that wiped out the private savings of millions, rampant lawlessness, a public health crisis, and a sharp decline in life expectancy and birth rates.

Sadly, this neoliberal “market reform” policy package that was introduced at a Stalin-like pace from 1992 to late 1998 was not only condoned but partly designed and financed by senior Clinton Administration officials, neoliberal economists, and innumerable USAID, World Bank, and IMF officials. The few dissenting voices included some of the West’s best economic brains—Nobel laureates like James Tobin, Kenneth Arrow, Lawrence Klein, and Joseph Stiglitz. They also included Moscow University’s Sergei Glaziev, who now serves as President Putin’s chief economic advisor.3 Unfortunately, they were no match for the folks with the cash.

There was also an important intervention in Russian politics. In January 1996 a secret team of professional U.S. political consultants arrived in Moscow to discover that, as CNN put it back then, “The only thing voters like less than Boris Yeltsin is the prospect of upheaval.” The experts’ solution was one of earliest “Our brand is crisis” campaign strategies, in which Yeltsin was “spun” as the only alternative to “chaos.” To support him, in March 1996 the IMF also pitched in with $10.1 billion of new loans, on top of $17.3 billion of IMF/World Bank loans that had already been made.

With all this outside help, plus ample contributions from Russia’s new elite, Yeltsin went from just 8 percent approval in the January 1996 polls to a 54-41 percent victory over the Communist Party candidate, Gennady Zyuganov, in the second round of the July 1996 election. At the time, mainstream media like Time and the New York Times were delighted. Very few outside Russia questioned the wisdom of this blatant intervention in post-Soviet Russia’s first democratic election, or the West’s right to do it in order to protect itself.

By the late 1990s the actual chaos that resulted from Yeltsin’s warped policies had laid the foundations for a strong counterrevolution, including the rise of ex-KGB officer Putin and a massive outpouring of oligarchic flight capital that has continued virtually up to the present. For ordinary Russians, as noted, this was disastrous. But for many banks, private bankers, hedge funds, law firms, and accounting firms, for leading oil companies like ExxonMobil and BP, as well as for needy borrowers like the Trump Organization, the opportunity to feed on post-Soviet spoils was a godsend. This was vulture capitalism at its worst.

The nine-lived Trump, in particular, had just suffered a string of six successive bankruptcies. So the massive illicit outflows from Russia and oil-rich FSU members like Kazahkstan and Azerbaijan from the mid-1990s provided precisely the kind of undiscriminating investors that he needed. These outflows arrived at just the right time to fund several of Trump’s post-2000 high-risk real estate and casino ventures—most of which failed. As Donald Trump, Jr., executive vice president of development and acquisitions for the Trump Organization, told the “Bridging U.S. and Emerging Markets Real Estate” conference in Manhattan in September 2008 (on the basis, he said, of his own “half dozen trips to Russia in 18 months”):

[I]n terms of high-end product influx into the United States, Russians make up a pretty disproportionate cross-section of a lot of our assets; say in Dubai, and certainly with our project in SoHo and anywhere in New York. We see a lot of money pouring in from Russia.

All this helps to explain one of the most intriguing puzzles about Donald Trump’s long, turbulent business career: how he managed to keep financing it, despite a dismal track record of failed projects.4

According to the “official story,” this was simply due to a combination of brilliant deal-making, Trump’s gold-plated brand, and raw animal spirits—with $916 million of creative tax dodging as a kicker. But this official story is hokum. The truth is that, since the late 1990s, Trump was also greatly assisted by these abundant new sources of global finance, especially from “submerging markets” like Russia

This suggests that neither Trump nor Putin is an “uncaused cause.” They are not evil twins, exactly, but they are both byproducts of the same neoliberal policy scams that were peddled to Russia’s struggling new democracy.

A Guided Tour of Trump’s Russian/FSU Connections

The following roundup of Trump’s Russo-Soviet business connections is based on published sources, interviews with former law enforcement staff and other experts in the United States, the United Kingdom, and Iceland, searches of online corporate registries,5 and a detailed analysis of offshore company data from the Panama Papers.6 Given the sheer scope of Trump’s activities, there are undoubtedly other worthy cases, but our interest is in overall patterns.

Note that none of the activities and business connections related here necessarily involved criminal conduct. While several key players do have criminal records, few of their prolific business dealings have been thoroughly investigated, and of course they all deserve the presumption of innocence. Furthermore, several of these players reside in countries where activities like bribery, tax dodging, and other financial chicanery are either not illegal or are rarely prosecuted. As former British Chancellor of the Exchequer Denis Healey once said, the difference between “legal” and “illegal” is often just “the width of a prison wall.”

So why spend time collecting and reviewing material that either doesn’t point to anything illegal or in some cases may even be impossible to verify? Because, we submit, the mere fact that such assertions are widely made is of legitimate public interest in its own right. In other words, when it comes to evaluating the probity of senior public officials, the public has the right to know about any material allegations—true, false, or, most commonly, unprovable—about their business partners and associates, so long as this information is clearly labeled as unverified.

Furthermore, the individual case-based approach to investigations employed by most investigative journalists and law enforcement often misses the big picture: the global networks of influence and finance, licit and illicit, that exist among business people, investors, kleptocrats, organized criminals, and politicians, as well as the “enablers”—banks, accounting firms, law firms, and havens. Any particular component of these networks might easily disappear without making any difference. But the networks live on. It is these shadowy transnational networks that really deserve scrutiny.

Bayrock Group LLC—Kazakhstan and Tevfik Arif

We’ll begin our tour of Trump’s Russian/FSU connections with several business relationships that evolved out of the curious case of Bayrock Group LLC, a spectacularly unsuccessful New York real estate development company that surfaced in the early 2000s and, by 2014, had all but disappeared except for a few lawsuits. As of 2007, Bayrock and its partners reportedly had more than $2 billion of Trump-branded deals in the works. But most of these either never materialized or were miserable failures, for reasons that will soon become obvious.

Bayrock’s “white elephants” included the 46-story Trump SoHo condo-hotel on Spring Street in New York City, for which the principle developer was a partnership formed by Bayrock and FL Group, an Icelandic investment company. Completed in 2010, the SoHo soon became the subject of prolonged civil litigation by disgruntled condo buyers. The building was foreclosed by creditors and resold in 2014 after more than $3 million of customer down payments had to be refunded. Similarly, Bayrock’s Trump International Hotel & Tower in Fort Lauderdale was foreclosed and resold in 2012, while at least three other Trump-branded properties in the United States, plus many other “project concepts” that Bayrock had contemplated, from Istanbul and Kiev to Moscow and Warsaw, also never happened.

Carelessness about due diligence with respect to potential partners and associates is one of Donald Trump’s more predictable qualities. Acting on the seat of the pants, he had hooked up with Bayrock rather quickly in 2005, becoming an 18 percent minority equity partner in the Trump SoHo, and agreeing to license his brand and manage the building.7

Exhibit A in the panoply of former Trump business partners is Bayrock’s former Chairman, Tevfik Arif (aka Arifov), an émigré from Kazakhstan who reportedly took up residence in Brooklyn in the 1990s. Trump also had extensive contacts with another key Bayrock Russian-American from Brooklyn, Felix Sater (aka Satter), discussed below.8 Trump has lately had some difficulty recalling very much about either Arif or Sater. But this is hardly surprising, given what we now know about them. Trump described his introduction to Bayrock in a 2013 deposition for a lawsuit that was brought by investors in the Fort Lauderdale project, one of Trump’s first with Bayrock: “Well, we had a tenant in … Trump Tower called Bayrock, and Bayrock was interested in getting us into deals.”9

According to several reports, Tevfik Arif was originally from Kazakhstan, a Soviet republic until 1992. Born in 1950, Arif worked for 17 years in the Soviet Ministry of Commerce and Trade, serving as Deputy Director of Hotel Management by the time of the Soviet Union’s collapse.10 In the early 1990s he relocated to Turkey, where he reportedly helped to develop properties for the Rixos Hotel chain. Not long thereafter he relocated to Brooklyn, founded Bayrock, opened an office in the Trump Tower, and started to pursue projects with Trump and other investors.11

Tevfik Arif was not Bayrock’s only connection to Kazakhstan. A 2007 Bayrock investor presentation refers to Alexander Mashevich’s “Eurasia Group” as a strategic partner for Bayrock’s equity finance. Together with two other prominent Kazakh billionaires, Patokh Chodiev (aka “Shodiyev”) and Alijan Ibragimov, Mashkevich reportedly ran the “Eurasian Natural Resources Cooperation.” In Kazakhstan these three are sometimes referred to as “the Trio.”12

The Trio has apparently worked together ever since Gorbachev’s late 1980s perestroika in metals and other natural resources. It was during this period that they first acquired a significant degree of control over Kazakhstan’s vast mineral and gas reserves. Naturally they found it useful to become friends with Nursultan Nazarbayev, Kazakhstan’s long-time ruler. Indeed, State Department cables leaked by Wikileaks in November 2010 describe a close relationship between “the Trio” and the seemingly-perpetual Nazarbayev kleptocracy.

In any case, the Trio has recently attracted the attention of many other investigators and news outlets, including the September 11 Commission Report, the Guardian, Forbes, and the Wall Street Journal. In addition to resource grabbing, the litany of the Trio’s alleged activities include money laundering, bribery, and racketeering.13 In 2005, according to U.S. State Department cables released by Wikileaks, Chodiev (referred to in a State Department cable as “Fatokh Shodiyev”) was recorded on video attending the birthday of reputed Uzbek mob boss Salim Abduvaliyeva and presenting him with a $10,000 “gift” or “tribute.”

According to the Belgian newspaper Le Soir, Chodiev and Mashkevich also became close associates of a curious Russian-Canadian businessman, Boris J. Birshtein. who happens to have been the father-in-law of another key Russian-Canadian business associate of Donald Trump in Toronto. We will return to Birshtein below.

The Trio also turn up in the April 2016 Panama Papers database as the apparent beneficial owners of a Cook Islands company, “International Financial Limited.”14The Belgian newspapers Het Laatste Nieuws, Le Soir, and La Libre Belgique have reported that Chodiev paid €23 million to obtain a “Class B” banking license for this same company, permitting it to make international currency trades. In the words of a leading Belgian financial regulator, that would “make all money laundering undetectable.”

The Panama Papers also indicate that some of Arif’s connections at the Rixos Hotel Group may have ties to Kazakhstan. For example, one offshore company listed in the Panama Papers database, “Group Rixos Hotel,” reportedly acts as an intermediary for four BVI offshore companies.15 Rixos Hotel’s CEO, Fettah Tamince, is listed as having been a shareholder for two of these companies, while a shareholder in another—“Hazara Asset Management”—had the same name as the son of a recent Kazakhstan Minister for Sports and Tourism. As of 2012, this Kazakh official was described as the third-most influential deputy in the country’s Mazhilis (the lower house of Parliament), in a Forbes-Kazakhstan article.

According to a 2015 lawsuit against Bayrock by Jody Kriss, one of its former employees, Bayrock started to receive millions of dollars in equity contributions in 2004, supposedly by way of Arif’s brother in Russia, who allegedly “had access to cash accounts at a chromium refinery in Kazakhstan.”

This as-yet unproven allegation might well just be an attempt by the plaintiff to extract a more attractive settlement from Bayrock and its original principals. But it is also consistent with fact that chromium is indeed one of the Kazakh natural resources that is reportedly controlled by the Trio.

As for Arif, his most recent visible brush with the law came in 2010, when he and other members of Bayrock’s Eurasian Trio were arrested together in Turkey during a police raid on a suspected prostitution ring, according to the Israeli daily Yediot Ahronot.

At the time, Turkish investigators reportedly asserted that Arif might be the head of a criminal organization that was trafficking in Russian and Ukrainian escorts, allegedly including some as young as 13.16 According to these assertions, big-ticket clients were making their selections by way of a modeling agency website, with Arif allegedly handling the logistics. Especially galling to Turkish authorities, the preferred venue was reportedly a yacht that had once belonged to the widely-revered Turkish leader Atatürk. It was also alleged that Arif may have also provided lodging for young women at Rixos Group hotels.17

According to Russian media, two senior Kazakh officials were also arrested during this incident, although the Turkish Foreign Ministry quickly dismissed this allegation as “groundless.” In the end, all the charges against Arif resulting from this incident were dismissed in 2012 by Turkish courts, and his spokespeople have subsequently denied all involvement.

Finally, despite Bayrock’s demise and these other legal entanglements, Arif has apparently remained active. For example, Bloomberg reports that, as of 2013, he, his son, and Rixos Hotels’ CEO Fettah Tamince had partnered to pursue the rather controversial business of advancing funds to cash-strapped high-profile soccer players in exchange for a share of their future marketing revenues and team transfer fees. In the case of Arif and his partners, this new-wave form of indentured servitude was reportedly implemented by way of a UK- and Malta-based hedge fund, Doyen Capital LLP. Because this practice is subject to innumerable potential abuses, including the possibility of subjecting athletes or clubs to undue pressure to sign over valuable rights and fees, UEFA, Europe’s governing soccer body, wants to ban it. But FIFA, the notorious global football regulator, has been customarily slow to act. To date, Doyen Capital LLP has reportedly taken financial gambles on several well-known players, including the Brazilian star Neymar.

The Case of Bayrock LLC—Felix Sater

Our second exhibit is Felix Sater, the senior Bayrock executive introduced earlier. This is the fellow who worked at Bayrock from 2002 to 2008 and negotiated several important deals with the Trump Organization and other investors. When Trump was asked who at Bayrock had brought him the Fort Lauderdale project in the 2013 deposition cited above, he replied: “It could have been Felix Sater, it could have been—I really don’t know who it might have been, but somebody from Bayrock.”18

Although Sater left Bayrock in 2008, by 2010 he was reportedly back in Trump Tower as a “senior advisor” to the Trump Organization—at least on his business card—with his own office in the building.

Sater has also testified under oath that he had escorted Donald Trump, Jr. and Ivanka Trump around Moscow in 2006, had met frequently with Donald over several years, and had once flown with him to Colorado. And although this might easily have been staged, he is also reported to have visited Trump Tower in July 2016 and made a personal $5,400 contribution to Trump’s campaign.

Whatever Felix Sater has been up to recently, the key point is that by 2002, at the latest,19 Tevfik Arif decided to hire him as Bayrock’s COO and managing director. This was despite the fact that by then Felix had already compiled an astonishing track record as a professional criminal, with multiple felony pleas and convictions, extensive connections to organized crime, and—the ultimate prize—a virtual “get out of jail free card,” based on an informant relationship with the FBI and the CIA that is vaguely reminiscent of Whitey Bulger.20

Sater, a Brooklyn resident like Arif, was born in Russia in 1966. He reportedly emigrated with his family to the United States in the mid-1970s and settled in “Little Odessa.” It seems that his father, Mikhael Sheferovsky (aka Michael Sater), may have been engaged in Russian mob activity before he arrived in the United States. According to a certified U.S. Supreme Court petition, Felix Sater’s FBI handler stated that he “was well familiar with the crimes of Sater and his (Sater’s) father, a (Semion) Mogilevich crime syndicate boss.”21 A 1998 FBI report reportedly said Mogilevich’s organization had “approximately 250 members,” and was involved in trafficking nuclear materials, weapons, and more, as well as money laundering. (See below.)

But Michael Sater may have been less ambitious than his son. His only reported U.S. criminal conviction came in 2000, when he pled guilty to two felony counts for extorting Brooklyn restaurants, grocery stores, and clinics. He was released with three years’ probation. Interestingly, the U.S. Attorney for the Eastern District of New York who handled that case at the time was Loretta Lynch, who succeeded Eric Holder as U.S. Attorney General in 2014. Back in 2000, she was also overseeing a budding informant relationship and a plea bargain with Michael’s son Felix, which may help to explain the father’s sentence.

By then young Felix Sater was already well on his way to a career as a prototypical Russian-American mobster. In 1991 he stabbed a commodity trader in the face with a margarita glass stem in a Manhattan bar, severing a nerve. He was convicted of a felony and sent to prison. As Trump tells it, Sater simply “got into a barroom fight, which a lot of people do.” The sentence for this felony conviction could not have been very long, because, by 1993, 27-year-old Felix was already a trader in a brand new Brooklyn-based commodity firm called “White Rock Partners,” an innovative joint venture among four New York crime families and the Russian mob aimed at bringing state-of-the art financial fraud to Wall Street.

Five years later, in 1998, Felix Sater pled guilty to stock racketeering, as one of 19 U.S.-and Russian mob-connected traders who participated in a $40 million “pump and dump” securities fraud scheme. Facing twenty years in Federal prison, Sater and Gennady Klotsman, a fellow Russian-American who’d been with him on the night of the Manhattan bar fight, turned “snitch” and helped the Department of Justice prosecute their co-conspirators.22 Reportedly, so did Salvatore Lauria, another “trader” involved in the scheme. According to the Jody Kriss lawsuit, Lauria later joined Bayrock as an off-the-books paid “consultant.” Initially their cooperation, which lasted from 1998 until at least late 2001, was kept secret, until it was inadvertently revealed in a March 2000 press release by U.S. Attorney Lynch.

Unfortunately for Sater, about the same time the NYPD also reportedly discovered that he had been running a money-laundering scheme and illicit gun sales out of a Manhattan storage locker. He and Klotsman fled to Russia. However, according to the New York Times, which cited Klotsman and Lauria, soon after the events of September 11, 2001, the ever-creative Sater succeeded in brokering information about the black market for Stinger anti-aircraft missiles to the CIA and the FBI. According to Klotsman, this strategy “bought Felix his freedom,” allowing him to return to Brooklyn. It is still not clear precisely what information Sater actually provided, but in 2015 U.S. Attorney General Loretta Lynch publicly commended him for sharing information that she described as “crucial to national security.”

Meanwhile, Sater’s sentence for his financial crimes continued to be deferred even after his official cooperation in that case ceased in late 2001. His files remained sealed, and he managed to avoid any sentencing for those crimes at all until October 23, 2009. When he finally appeared before the Eastern District’s Judge I. Leo Glasser, Felix received a $25,000 fine, no jail time, and no probation in a quiet proceeding that attracted no press attention. Some compared this sentence to Judge Glasser’s earlier sentence of Mafia hit man “Sammy the Bull” Gravano to 4.5 years for 19 murders, in exchange for “cooperating against John Gotti.”

In any case, between 2002 and 2008, when Felix Sater finally left Bayrock LLC, and well beyond, his ability to avoid jail and conceal his criminal roots enabled him to enjoy a lucrative new career as Bayrock’s chief operating officer. In that position, he was in charge of negotiating aggressive property deals all over the planet, even while—according to lawsuits by former Bayrock investors—engaging in still more financial fraud. The only apparent difference was that he changed his name from “Sater” to “Satter.”23

In the 2013 deposition cited earlier, Trump went on to say “I don’t see Felix as being a member of the Mafia.” Asked if he had any evidence for this claim, Trump conceded “I have none.”24

As for Sater’s pal Klotsman, the past few years have not been kind. As of December 2016 he is in a Russian penal colony, working off a ten-year sentence for a failed $2.8 million Moscow diamond heist in August 2010. In 2016 Klotsman was reportedly placed on a “top-ten list” of Americans that the Russians were willing to exchange for high-value Russian prisoners in U.S. custody, like the infamous arms dealer Viktor Bout. So far there have been no takers. But with Donald Trump as President, who knows?

The Case of Iceland’s FL Group

One of the most serious frauds alleged in the recent Bayrock lawsuit involves FL Group, an Icelandic private investment fund that is really a saga all its own.

Iceland is not usually thought of as a major offshore financial center. It is a small snowy island in the North Atlantic, closer to Greenland than to the UK or Europe, with only 330,000 citizens and a total GDP of just $17 billion. Twenty years ago, its main exports were cod and aluminum—with the imported bauxite smelted there to take advantage of the island’s low electricity costs.

But in the 1990s Iceland’s tiny neoliberal political elite had what they all told themselves was a brilliant idea: “Let’s privatize our state-owned banks, deregulate capital markets, and turn them loose on the world!” By the time all three of the resulting privatized banks, as well as FL Group, failed in 2008, the combined bank loan portfolio amounted to more than 12.5 times Iceland’s GDP—the highest country debt ratio in the entire world.

For purposes of our story, the most interesting thing about Iceland is that, long before this crisis hit and utterly bankrupted FL Group, our two key Russian/FSU/Brooklyn mobster-mavens, Arif and Sater, had somehow stumbled on this obscure Iceland fund. Indeed, in early 2007 they persuaded FL Group to invest $50 million in a project to build the Trump SoHo in mid-town Manhattan.

According to the Kriss lawsuit, at the same time, FL Group and Bayrock’s Felix Sater also agreed in principle to pursue up to an additional $2 billion in other Trump-related deals. The Kriss lawsuit further alleges that FL Group (FLG) also agreed to work with Bayrock to facilitate outright tax fraud on more than $250 million of potential earnings. In particular, it alleges that FLG agreed to provide the $50 million in exchange for a 62 percent stake in the four Bayrock Trump projects, but Bayrock would structure the contract as a “loan.” This meant that Bayrock would not have to pay taxes on the initial proceeds, while FLG’s anticipated $250 million of dividends would be channeled through a Delaware company and characterized as “interest payments,” allowing Bayrock to avoid up to $100 million in taxes. For tax purposes, Bayrock would pretend that their actual partner was a Delaware partnership that it had formed with FLG, “FLG Property I LLC,” rather than FLG itself.

The Trump Organization has denied any involvement with FLG. However, as an equity partner in the Trump SoHo, with a significant 18 percent equity stake in this one deal alone, Donald Trump himself had to sign off on the Bayrock-FLG deal.

This raises many questions. Most of these will have to await the outcome of the Kriss litigation, which might well take years, especially now that Trump is President. But several of these questions just leap off the page.

First, how much did President-elect Trump know about the partners and the inner workings of this deal? After all, he had a significant equity stake in it, unlike many of his “brand-name only” deals, and it was also supposed to finance several of his most important East Coast properties.

Second, how did the FL Group and Bayrock come together to do this dodgy deal in the first place? One former FL Group manager alleges that the deal arrived by accident, a “relatively small deal” was nothing special on either side.25 The Kriss lawsuit, on the other hand, alleges that FLG was a well-known source of easy money from dodgy sources like Kazakhstan and Russia, and that other Bayrock players with criminal histories—like Salvatore Lauria, for example—were involved in making the introductions.

At this stage the evidence with respect to this second question is incomplete. But there are already some interesting indications that FL Group’s willingness to generously finance Bayrock’s peculiar Russian/FSU/Brooklyn team, its rather poorly-conceived Trump projects, and its purported tax dodging were not simply due to Icelandic backwardness. There is much more for us to know about Iceland’s “special” relationship with Russian finance. In this regard, there are several puzzles to be resolved.

First, it turns out that FL Group, Iceland’s largest private investment fund until it crashed in 2008, had several owners/investors with deep Russian business connections, including several key investors in all three top Iceland banks.

Second, it turns out that FL Group had constructed an incredible maze of cross-shareholding, lending, and cross-derivatives relationships with all these major banks, as illustrated by the following snapshot of cross-shareholding among Iceland’s financial institutions and companies as of 2008.

This thicket of cross-dealing made it almost impossible to regulate “control fraud,” where insiders at leading financial institutions went on a self-serving binge, borrowing and lending to finance risky investments of all kinds. It became difficult to determine which institutions were net borrowers or investors, as the concentration of ownership and self-dealing in the financial system just soared.

Third, FL Group make a variety of peculiar loans to Russian-connected oligarchs as well as to Bayrock. For example, as discussed below, Alex Shnaider, the Russian-Canadian billionaire who later became Donald Trump’s Toronto business partner, secured a €45.8 million loan to buy a yacht from Kaupthing Bank during the same period, while a company belonging to another Russian billionaire who reportedly owns an important vodka franchise got an even larger loan.27

Fourth, Iceland’s largest banks also made a series of extraordinary loans to Russian interests during the run-up to the 2008 crisis. For example, one of Russia’s wealthiest oligarchs, a close friend of President Putin, nearly managed to secure at least €400 million (or, some say, up to four times that much) from Kaupthing, Iceland’s largest bank, in late September 2008, just as the financial crisis was breaking wide open. This bank also had important direct and indirect investments in FL Group. Indeed, until December 2006, it is reported to have employed the FL Group private equity manager who allegedly negotiated Felix Sater’s $50 million deal in early 2007.28

Fifth, there are unconfirmed accounts of a secret U.S. Federal Reserve report that unnamed Iceland banks were being used for Russian money laundering.29Furthermore, Kaupthing Bank’s repeated requests to open a New York branch in 2007-08 were rejected by the Fed. Similar unconfirmed rumors repeatedly appeared in Danish and German publications, as did allegations about the supposed Kazakh origins of FLG’s cash to be “laundered” in the Kriss lawsuit.

Sixth, there is the peculiar fact that, when Iceland’s banks went belly-up in October 2008, their private banking subsidiaries in Luxembourg, which were managing at least €8 billion of private assets, were suddenly seized by Luxembourg banking authorities and transferred to a new bank, Banque Havilland. This happened so fast that Iceland’s Central Bank was prevented from learning anything about the identities or portfolio sizes of the Iceland banks’ private offshore clients. But again, there were rumors of some important Russian names.

Finally, there is the rather odd phone call that Russia’s Ambassador to Iceland made to Iceland’s Prime Minister at 6:45 a.m. on October 7, 2008, the day after the financial crisis hit Iceland. According to the PM’s own account, the Russian Ambassador informed him that then-Prime Minister Putin was willing to consider offering Iceland a €4 billion Russian bailout.

Of course this alleged Putin offer was modified not long thereafter into a willingness to entertain an Icelandic negotiating team in Moscow. By the time the Iceland team got to Moscow later that year, Russia’s desire to lend had cooled, and Iceland ended up accepting a $2.1 billion IMF “stabilization package” instead. But according to a member of the negotiating team, the reasons for the reversal are still a mystery. Perhaps Putin had reconsidered because he simply decided that Russia had to worry about its own considerable financial problems. Or perhaps he had discovered that Iceland’s banks had indeed been very generous to Russian interests on the lending side, while—given Luxembourg’s actions—any Russian private wealth invested in Icelandic banks was already safe.

On the other hand, there may be a simpler explanation for Iceland’s peculiar generosity to sketchy partners like Bayrock. After all, right up to the last minute before the October 2008 meltdown, the whole world had awarded Iceland AAA ratings: Depositors queued up in London to open high-yield Iceland bank accounts, its bank stocks were booming, and the compensation paid to its financiers was off the charts. So why would anyone worry about making a few more dubious deals?

Overall, therefore, with respect to these odd “Russia-Iceland” connections, the proverbial jury is still out. But all these Icelandic puzzles are intriguing and bear further investigation.

The Case of the Trump Toronto Tower and Hotel—Alex Shnaider

Our fourth case study of Trump’s business associates concerns the 48-year-old Russian-Canadian billionaire Alex Shnaider, who co-financed the seventy-story Trump Tower and Hotel, Canada’s tallest building. It opened in Toronto in 2012. Unfortunately, like so many of Trump’s other Russia/FSU-financed projects, this massive Toronto condo-hotel project went belly-up this November and has now entered foreclosure.

According to an online profile of Shnaider by a Ukrainian news agency, Alex Shnaider was born in Leningrad in 1968, the son of “Евсей Шнайдер,” or “Evsei Shnaider” in Russian.30 A recent Forbes article says that he and his family emigrated to Israel from Russia when he was four and then relocated to Toronto when he was 13-14. The Ukrainian news agency says that Alex’s familly soon established “one of the most successful stories in Toronto’s Russian quarter, “ and that young Alex, with “an entrepreneurial streak,” “helped his father Evsei Shnaider in the business, placing goods on the shelves and wiping floors.”

Eventually that proved to be a great decision—Shnaider prospered in the New World. Much of this was no doubt due to raw talent. But it also appears that for a time he got significant helping hand from his (now reportedly ex-) father-in-law, another colorful Russian-Canadian, Boris J. Birshtein.

Originally from Lithuania, Birshtein, now about 69, has been a Canadian citizen since at least 1982.31 He resided in Zurich for a time in the early 1990s, but then returned to Toronto and New York.32 One of his key companies was called Seabeco SA, a “trading” company that was registered in Zurich in December 1982.33 By the early 1990s Birshtein and his partners had started many other Seabeco-related companies in a wide variety of locations, inclding Antwerp,34 Toronto,35Winnipeg,36 Moscow, Delaware,37 Panama,38 and Zurich.39 Several of these are still active.40 He often staffed them with directors and officers from a far-flung network of Russians, emissaries from other FSU countries like Kyrgyzstan and Moldova, and recent Russia/FSU emigres to Canada.41

According to the Financial Times and the FBI, in addition to running Seabeco, Birshtein was a close business associate of Sergei Mikhaylov, the reputed head of Solntsevskaya Bratva, the Russian mob’s largest branch, and the world’s highest-grossing organized crime group as of 2014, according to Fortune.42 A 1996 FBI intelligence report cited by the FT claims that Birshtein hosted a meeting in his Tel Aviv office for Mikhaylov, the Ukrainian-born Semion Mogilevich, and several other leaders of the Russo/FSU mafia, in order to discuss “sharing interests in Ukraine.”43 A subsequent 1998 FBI Intelligence report on the “Semion Mogilevich Organization” repeated the same charge,44 and described Mogilevich’s successful attempts at gaining control over Ukraine privatization assets. The FT article also described how Birshtein and his associates had acquired extraordinary influence with key Ukraine officials, including President Leonid Kuchma, with the help of up to $5 million of payoffs.45 Citing Swiss and Belgian investigators, the FT also claimed that Birshtein and Mikhaylov jointly controlled a Belgian company called MAB International in the early 1990s.46 During that period, those same investigators reportedly observed transfers worth millions of dollars between accounts held by Mikhaylov, Birshtein, and Alexander Volkov, Seabeco’s representative in Ukraine.

In 1993, the Yeltsin government reportedly accused Birshtein of illegally exporting seven million tons of Russian oil and laundering the proceeds.47Dmytro Iakoubovski, a former associate of Birshtein’s who had also moved to Toronto, was said to be cooperating with the Russian investigation. One night a gunman fired three shots into Iakoubovski’s home, leaving a note warning him to cease his cooperation, according to a New York Times article published that year. As noted above, according to the Belgian newspaper Le Soir, two members of Bayrock’s Eurasian Trio were also involved in Seabeco during this period as well—Patokh Chodiev and Alexander Mashkevich. Chodiev reportedly first met Birshtein through the Soviet Foreign Ministry, and then went on to run Seabeco’s Moscow office before joining its Belgium office in 1991. Le Soir further claims that Mashkevich worked for Seabeco too, and that this was actually how he and Chodiev had first met.

All this is fascinating, but what about the connections between Birshtein and Trump’s Toronto business associate, Alex Shnaider? Again, the leads we have are tantalizing.The Toronto Globe and Mail reported that in 1991, while enrolled in law school, young Alex Shnaider started working for Birshtein at Seabeco’s Zurich headquarters, where he was reportedly introduced to steel trading. Evidently this was much more than just a job; the Zurich company registry lists “Alex Shnaider” as a director of “Seabeco Metals AG” from March 1993 to January 1994.48

In 1994, according to this account, he reportedly left Seabeco in January 1994 to start his own trading company in Antwerp, in partnership with a Belgian trader-partner. Curiously, Le Soir also says that Mikhaylov and Birshtein co-founded MAB International in Antwerp in January 1994. Is it far-fetched to suspect that Alex Shnaider and mob boss Mikhaylov might have crossed paths, since they were both in the same city and they were both close to Shnaider’s father-in-law?

According to Forbes, soon after Shnaider moved to Antwerp, he started visiting the factories of his steel trading partners in Ukraine.49 His favorite client was the Zaporizhstal steel mill, Ukraine’s fourth largest. At the Zaporizhstal mill he reportedly met Eduard Shifrin (aka Shyfrin), a metals trader with a doctorate in metallurgical engineering. Together they founded Midland Resource Holdings Ltd. in 1994.50

As the Forbes piece argues, with privatization sweeping Eastern Europe, private investors were jockeying to buy up the government’s shares in Zaprozhstal. But most traders lacked the financial backing and political connectons to accumulate large risky positions. Shnaider and Shifrin, in contrast, started buying up shares without limit, as if their pockets and connections were very deep. By 2001 they had purchased 93 percent of the plant for about $70 million, a stake that would be worth much more just five years later, when Shnaider reportedly turned down a $1.2 billion offer.

Today, Midland Resources Holdings Ltd. reportedly generates more than $4 billion a year of revenue and has numerous subsidiaries all across Eastern Europe.51 Shnaider also reportedly owns Talon International Development, the firm that oversaw construction of the Trump hotel-tower in Toronto. All this wealth apparently helped Iceland’s FL Group decide that it could afford to extend a €45.8 million loan to Alex Shnaider in 2008 to buy a yacht.52

As of December 2016, a search of the Panama Papers database found no fewer than 28 offshore companies that have been associated with “Midland Resources Holding Limited.”53 According to the database, “Midland Resources Holding Limited” was a shareholder in at least two of these companies, alongside an individual named “Oleg Sheykhametov.”54 The two companies, Olave Equities Limited and Colley International Marketing SA, were both registered and active in the British Virgin Islands from 2007–10.55 A Russian restaurateur by that same name reportedly runs a business owned by two other alleged Solntsevskaya mob associates, Lev Kvetnoy and Andrei Skoch, both of whom appear with Sergei Mikhaylov. Of course mere inclusion in such a group photo is not evidence of wrongdoing. (See the photo here.) According to Forbes, Kvetnoy is the 55th richest person in Russia and Skoch, now a deputy in the Russian Duma, is the 18th.56

Finally, it is also intriguing to note that Boris Birshtein is also listed as the President of “ME Moldova Enterprises AG,” a Zurich-based company” that was founded in November 1992, transferred to the canton of Schwyz in September 1994, and liquidated and cancelled in January 1999.57 Birshstein was a member of the company’s board of directors from November 1992 to January 1994, when he became its President. At that point he was succeeded as President in June 1994 by one “Evsei Shnaider, Canadian citizen, resident in Zurich,” who was also listed as director of the company in September 1994.58 “Evsei Schnaider” is also listed in the Panama registry as a Treasurer and Director of “The Seabeco Group Inc.,” formed on December 6, 1991,59 and as treasurer and director of Seabeco Security International Inc.,” formed on December 10, 1991. As of December 2016, both companies are still in existence.60 Boris Birshtein is listed as president and director of both companies.61

The Case of Paul Manafort’s Ukrainian Oligarchs

Our fifth Trump associate profile concerns the Russo/Ukrainian connections of Paul Manafort, the former Washington lobbyist who served as Donald Trump’s national campaign director from April 2016 to August 2016. Manafort’s partner, Rick Davis, also served as national campaign manager for Senator John McCain in 2008, so this may not just be a Trump association.

One of Manafort’s biggest clients was the dubious pro-Russian Ukrainian billionaire Dmytro Firtash. By his own admission, Firtash maintains strong ties with a recurrent figure on this scene, the reputed Ukrainian/Russian mob boss Semion Mogilevich. His most important other links are almost certainly to Putin. Otherwise it is difficult to explain how this former used-car salesman could gain a lock on trading goods for gas in Turkmenistan and also become a lynchpin investor in the Swiss company RosUrEnergo, which controls Gazprom’s gas sales to Europe.62

In 2008, Manafort teamed up with a former manager of the Trump Organization to purchase the Drake Hotel in New York for up to $850 million, with Firtash agreeing to invest $112 million. According to a lawsuit brought against Manafort and Firtash, the key point of the deal was not to make a carefully-planned investment in real estate, but to simply launder part of the huge profits that Firtash had skimmed while brokering dodgy natural gas deals between Russia and Ukraine, with Mogilevich acting as a “silent partner.”

Ultimately Firtash pulled out of this Drake Hotel deal. The reasons are unclear—it has been suggested that he needed to focus on the 2015 collapse and nationalization of his Group DF’s Bank Nadra back home in Ukraine.63 But it certainly doesn’t appear to have changed his behavior. Since 2014 there has been a spate of other Firtash-related prosecutions, with the United States trying to extradict from Austria in order to stand trial on allegations that his vast spidernet “Group DF” had bribed Indian officials to secure mining licenses. The Austrian court has required him to put up a record-busting €125 million bail while he awaits a decision.64 And just last month, Spain has also tried to extradite Firtash on a separate money laundering case, involving the laundering of €10 million through Spanish property investments.

After Firtash pulled out of the deal, Manafort reportedly turned to Trump, but he declined to engage. Manafort stepped down as Trump’s campaign manager in August of 2016 in response to press investigations into his ties not only to Firtash, but to Ukraine’s previous pro-Russian Yanukovych government, which had been deposed by a uprising in 2014. However, following the November 8 election, Manafort reportedly returned to advise Trump on staffing his new administration. He got an assist from Putin—on November 30 a spokeswoman for the Russian Foreign Ministry accused Ukraine of leaking stories about Manafort in an effort to hurt Trump.

The Case of “Well-Connected” Russia/FSU Mobsters

Finally, several other interesting Russian/FSU connections have a more residential flavor, but they are a source of very important leads about the Trump network.

Indeed, partly because it has no prying co-op board, Trump Tower in New York has received press attention for including among its many honest residents tax-dodgers, bribers, arms dealers, convicted cocaine traffickers, and corrupt former FIFA officials.65

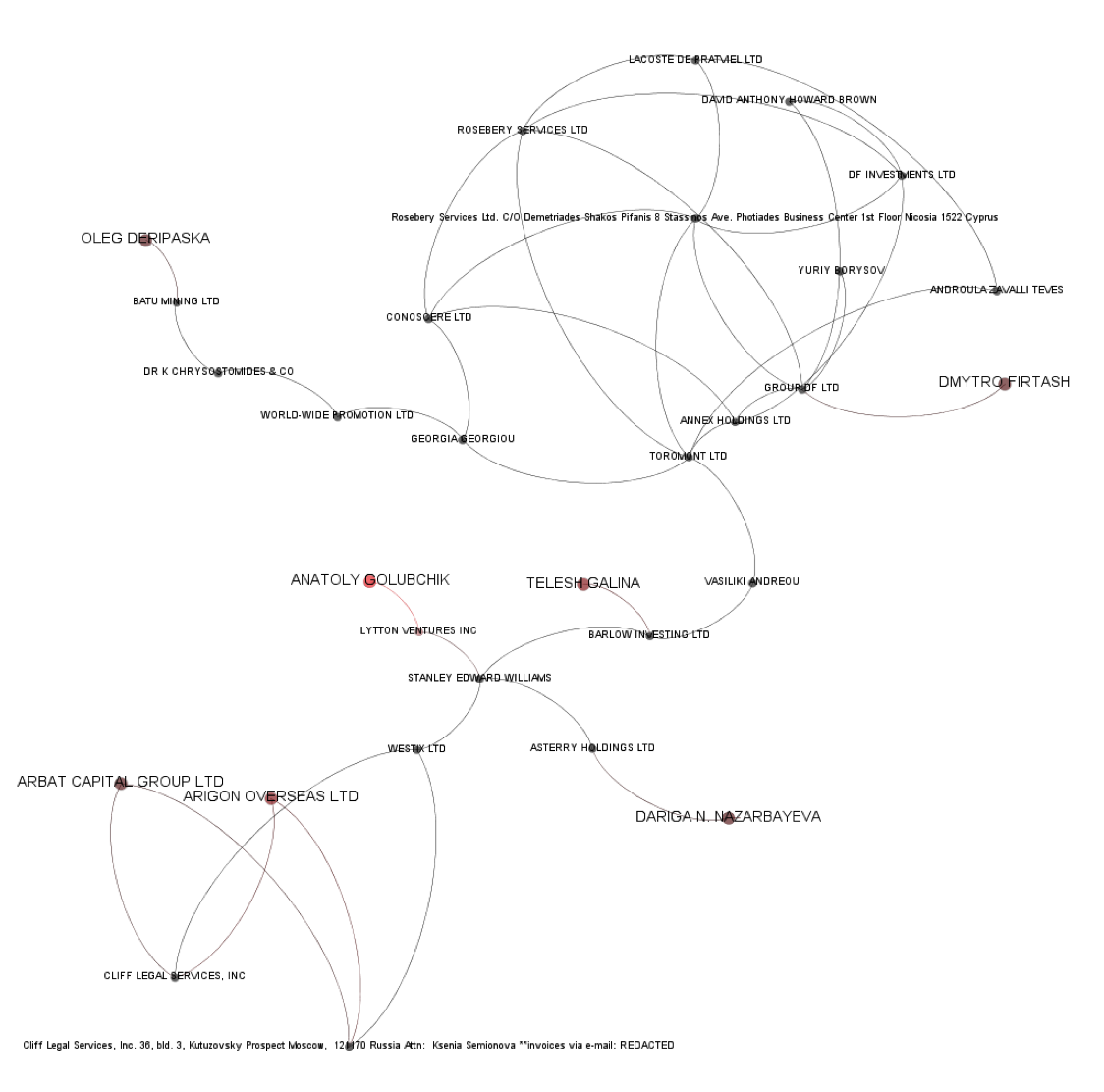

One typical example involves the alleged Russian mobster Anatoly Golubchik, who went to prison in 2014 for running an illegal gambling ring out of Trump Tower—not only the headquarters of the Trump Organization but also the former headquarters of Bayrock Group LLC. This operation reportedly took up the entire 51st floor. Also reportedly involved in it was the alleged mobster Alimzhan Tokhtakhounov,66 who has the distinction of making the Forbes 2008 list of the World’s Ten Most Wanted Criminals, and whose organization the FBI believes to be tied to Mogilevich’s. Even as this gambling ring was still operating in Trump Tower, Tokhtakhounov reportedly travelled to Moscow to attend Donald Trump’s 2013 Miss Universe contest as a special VIP.

In the Panama Papers database we do find the name “Anatoly Golubchik.” Interestingly, his particular offshore company, “Lytton Ventures Inc.,”67 shares a corporate director, Stanley Williams, with a company that may well be connected to our old friend Semion Mogilevich, the Russian mafia’s alleged “Boss of Bosses” who appeared so frequently in the story above. Thus Lytton Ventures Inc. shares this particular director with another company that is held under the name of “Galina Telesh.”68 According to the Organized Crime and Corruption Reporting Project, multiple offshore companies belonging to Semion Mogilevich have been registered under this same name—which just happens to be that of Mogilevich’s first wife.

A 2003 indictment of Mogilevich also mentions two offshore companies that he is said to have owned, with names that include the terms “Arbat” and “Arigon.” The same corporate director shared by Golubchik and Telesh also happens to be a director of a company called Westix Ltd.,69 which shares its Moscow address with “Arigon Overseas” and “Arbat Capital.”70 And another company with that same director appears to belong to Dariga Nazarbayeva, the eldest daughter of Nursultan Nazarbayev, the long-lived President of Kazakhstan. Dariga is expected to take his place if he ever decides to leave office or proves to be mortal.

Lastly, Dmytro Firtash—the Mogilevich pal and Manafort client that we met earlier—also turns up in the Panama Papers database as part of Galina Telesh’s network neighborhood. A director of Telesh’s “Barlow Investing,” Vasliki Andreou, was also a nominee director of a Cyprus company called “Toromont Ltd.,” while another Toromont Ltd. nominee director, Annex Holdings Ltd., a St. Kitts company, is also listed as a shareholder in Firtash’s Group DF Ltd., along with Firtash himself.71 And Group DF’s CEO, who allegedly worked with Manafort to channel Firtash’s funding into the Drake Hotel venture, is also listed in the Panama Papers database as a Group DF shareholder. Moreover, a 2006 Financial Times investigation identified three other offshore companies that are linked to both Firtash and Telesh.72

Of course, all of these curious rrelationships may just be meaningless coincidences. After all, the director shared by Telesh and Golubchik is also listed in the same role for more than 200 other companies, and more than a thousand companies besides Arbat Capital and Arigon Overseas share Westix’s corporate address. In the burgeoning land of offshore havens and shell-game corporate citizenship, there is no such thing as overcrowding. The appropriate way to view all this evidence is to regard it as “Socratic:” raising important unanswered questions, not providing definite answers.

In any case, returning to Trump’s relationships through Trump Tower, another odd one involves the 1990s-vintage fraudulent company YBM Magnex International. YBM, ostensibly a world-class manufacturer of industrial magnets, was founded indirectly in Newtown, Bucks County, Pennsylvania in 1995 by the “boss of bosses,” Semion Mogilevich, Moscow’s “brainy Don.”

This is a fellow with an incredible history, even if only half of what has been written about him is true.73 Unfortunately, we have to focus here only on the bits that are most relevant. Born in Kiev, and now a citizen of Israel as well as Ukraine and Russia, Semion, now seventy, is a lifelong criminal. But he boasts an undergraduate economics degree from Lviv University, and is reported to take special pride in designing sophisticated, virtually undetectable financial frauds that take years to put in place. To pull them off, he often relies on the human frailties of top bankers, stock brokers, accountants, business magnates, and key politicians.74

In YBM’s case, for a mere $2.4 million in bribes, Semion and his henchmen spent years in the 1990s launching a product-free, fictitious company on the still-badly under-regulated Toronto Stock Exchange. Along the way they succeeded in securing the support of several leading Toronto business people and a former Ontario Province Premier to win a seat on YBM’s board. They also paid the “Big Four” accounting firm Deloitte Touche very handsomely in exchange for glowing audits. By mid-1998, YBM’s stock price had gone from less than $0.10 to $20, and Semion cashed out at least $18 million—a relatively big fraud for its day—before the FBI raid its YBM’s corporate headquarters. When it did so, it found piles of bogus invoices for magnets, but no magnets.75

In 2003, Mogilevich was indicted in Philadelphia on 45 felony counts for this $150 million stock fraud. But there is no extradition treaty between the United States and Russia, and no chance that Russia will ever extradite Semion voluntarily; he is arguably a national treasure, especially now. Acknowledging these realities, or perhaps for other reasons, the FBI quietly removed Mogilevich from its Top Ten Most Wanted list in 2015, where he had resided for the previous six years.76

For our purposes, one of the most interesting things to note about this YBM Magnex case is that its CEO was a Russian-American named Jacob Bogatin, who was also indicted in the Philadelphia case. His brother David had served in the Soviet Army in a North Vietnamese anti-aircraft unit, helping to shoot down American pilots like Senator John McCain. Since the early 1990s, David Bogatin was considered by the FBI to be one of the key members of Semion Mogilevich’s Russian organized crime family in the United States, with a long string of convictions for big-ticket Mogilevich-type offenses like financial fraud and tax dodging.

At one point, David Bogatin owned five separate condos in Trump Tower that Donald Trump had reportedly sold to him personally.77 And Vyacheslav Ivankov, another key Mogilevich lieutenant in the United States during the 1990s, also resided for a time at Trump Tower, and reportedly had in his personal phone book the private telephone and fax numbers for the Trump Organization’s office in that building.78

After all, on September 1, 1987 (!), Trump was already willing to spend a $94,801 on full-page ads in the Boston Globe, the Washington Post, and the New York Times calling for the United States to stop spending money to defend Japan, Europe, and the Persian Gulf, “an area of only marginal significance to the U.S. for its oil supplies, but one upon which Japan and others are almost totally dependent.”79

This is one key reason why just this week, Robert Gates—a registered Republican who served as Secretary of Defense under Presidents Bush and Obama, as well as former Director and Deputy Director of the CIA—criticized the response of Congress and the White House to the alleged Putin-backed hacking as far too “laid back.”80

Unfortunately, for many reasons, this year American voters never really got the chance to decide whether such low connections and entanglements belong at the world’s high peak of official power. In the waning days of the Obama Administration, with the Electoral College about to ratify Trump’s election and Congress in recess, it is too late to establish the kind of bipartisan, 9/11-type commission that would be needed to explore these connections in detail.

1Author’s estimates; see globalhavenindustry.com for more details.

2For an overview and critical discussion, see here.

James S. Henry, Esq. is an investigative economist and lawyer who has written widely about offshore and onshore tax havens, kleptocracy, and pirate banking. He is the author of The Blood Bankers (Basic Books, 2003,2005), a classic investigation of where the money went that was loaned to key debtor countries in the 1970s-1990s. He is a senior fellow at the Columbia University’s Center on Sustainable Investment, a Global Justice Fellow at Yale, a senior advisor at the Tax Justice Network, and a member of the New York Bar. He has pursued frontline investigations of odious debt, flight capital, and corruption in more than fifty developing countries, including Russia, China, South Africa, Brazil, the Philippines, Argentina, Venezuela, and Panama.

No comments:

Post a Comment